Inventory management is a humungous task for all business corporations. For those into manufacturing and retailing, inventory management is a vital business function that determines their survival, profitability, and competitiveness in the market. There have been devised numerous techniques and software that claim to provide a perfect plan to effectively and efficiently manage this area.

Managing inventory is a delicate balancing act. It requires the organization to maintain a fine balance between maintaining optimum inventory levels always and avoiding ‘Stock out’ situations or obsolete inventory on one hand and avoiding investing too much of capital in stock on the other hand, which may entail heavy carrying costs of warehouse rentals and potential dangers of damages and obsolescence resulting into heavy losses for the business.

Hence, many techniques have proved useful for the managers in calculating optimum inventory levels and managing them throughout all the phases of business cycles and accounting periods. Here, we will discuss the ABC Analysis of Inventory management.

Table of Contents

What is ABC Analysis of Inventory Management?

ABC analysis of inventory management system is a way of inventory control based on their relatively high consumption value and frequency of use in order to determine which items are most important for your company.

The idea behind ABC analysis is that you have three classes of inventory: A, B, and C. You then assign each item in your inventory to one of these three categories based on its value, or how much the inventory cost to replace if you don’t have it in stock.

You also assign each item based on its frequency of use or customer demand: how often it’s used or needed by customers or employees in order for them to do their jobs.

Your A items are the ones that cost the most and are used the most—for example, raw materials that are used every day in production processes.

Your B items are those that cost less and are used less frequently—for example, office supplies that don’t need constant replenishment but are expensive enough that they should still be stocked at all times.

Your C items are those that cost the least and are used even less frequently—for example, spare parts for machines whose regular maintenance will keep them running without any issues for years without needing replacement parts.

The Genesis of ABC Analysis

Vilfredo Pareto, a renowned economist, has propagated this theory almost a century ago that 80% of the wealth in any society is held by 20% of its people. This principle got international acclaim as Pareto Principle or 80:20 Rule. It has also been applied to various other business and economic situations.

In 1940, a mechanical engineer named Joseph Juran derived ABC analysis classification from the Pareto Principle wherein he sought to segregate ‘Critical Few’ from ‘Trivial Many’ of the inventory items.

Pareto Principle for Inventory Management methods says that 80% of the historical sales data is derived from 20% of the stock items. ABC analysis works on the same principle and recommends the basis for ABC analysis classification and management of inventory.

Rule of ABC Analysis

ABC analysis classifies inventory into 3 categories:

Class A – forms 15% to 20% of the stock quantity but commands 80% to 85% of the total inventory value.

Class B – forms 30% to 35% of the stock quantity but commands 10% to 15% of the inventory value.

Class C – forms 50% of the stock in terms of quantity but commands only 55% of the inventory value.

Thus, it can be seen that Group A, which accounts for only a minor portion of the physical units, is very valuable in terms of the revenue it brings. Group B is ‘mid-range’ stock items that comprise a slightly larger share of the physical stock units but their value is still less as compared to Class A.

And finally, Class C items are a large collection of such small, insignificant items that are essential for running the business smoothly but their commercial value is inconsequential through ABC analysis.

Inventory Management Process

After classifying under Group A, B and C; the following principles can be followed for the management under each of the three groups:

Class A items should be managed very closely

The stocktaking under this category should be frequent (monthly) as these are quite valuable items for the business. Similarly, their reorder levels should be fixed at such time intervals so as to avoid the situation of running out of these crucial items. The business may think fit to allocate some personnel exclusively to look after this class.

This is because these items are principal revenue drivers for the business. Any incident of not having them in stock when there is a demand may result in opportunity loss for the business. There should always be sufficient stock levels of these items as the business is assured of the high turnout of this class and can afford to carry a large number of these units in stock.

Class B items are the items that a business should closely monitor

This is because they have the potential to move to Class A and become the highest-selling and valuable items of the business or their popularity may further drop and they may move to Class C where they have to be stocked but not always important.

In this case, periodical stock-taking (quarterly) is required. Also, their reorder levels should be adhered to. The business should seek to minimize the stock handling costs for this class of items but should closely observe their movement from Class B to either Class A or Class C. In fact, this is where a growth opportunity lies for a business.

Class A customers are the customers whose confidence has already been won by the business. Class B is dealing with the business but not very frequently and in significant volume. The business may analyze their needs, respond to their demands which were previously unmet, and convert Class B stock items into Class A – high sales, high volume – items.

Class C items are very low-value items that are not in high demand with the customers

Nonetheless, the business has to carry the stock of these items in order to respond to occasional demands and smooth business operations. Thus here, the stock carrying costs must be minimized.

This is because these items consist of almost 50% of the stock units and if the business carries them in large numbers, then the stock handling costs such as storage space rentals, salaries of warehouse staff, insurance charges would skyrocket. The SKUs (stock-keeping units) of this class should be always stored at minimum levels.

The stocktaking of these items can be done annually. The stocktaking procedures; reorder levels determination, and placing the order can be automated with very less management intervention. Some items from within this class may be on the decline in their Product Life Cycle curve and the business will have to ensure their discontinuance if the demand dies down completely.

Example of Calculation under Analysing

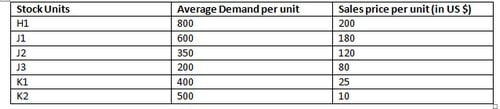

The following table contains various stock units for the business, their demand, and their sales price per unit:

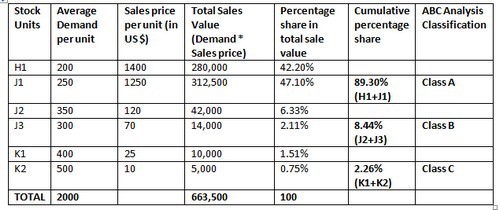

Now, we will work out the sales value of these units individually, the total sales value, and the total no. of units that the business has to stock.

Next, we will work out the percentage share of each category into the total sales value of US$ 339,000.

Finally, the composite percentage share of high value inventory items and their classification according to ABC analysis can be worked out:

Here, it can be seen that stock items H1 and J1 together control almost 90% share of the total sales value and hence have been classified as Group A which demands the highest attention, active management of inventory, and constant monitoring of these stock items.

J2 and J3 command 8.44% of the share in total sales value whereas K1 and K2 command a meager 2.26% of the total sales value. Hence, they have been categorized as Class B and Class C respectively.

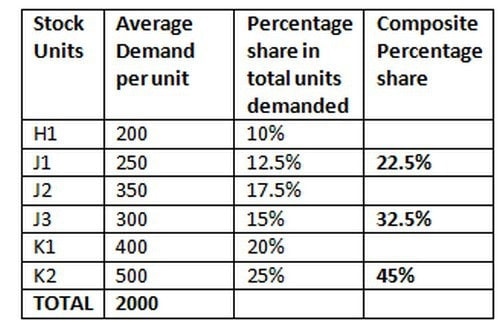

Now, if you see the percentage share of the units in each category with respect to the total units demanded, it would look like this:

The above-mentioned table shows clearly that:

- Class A items represent 22.5% of the total stock units and generate 89.30% of the revenue

- Class B items constitute 32.5% of the total stock units and generate 8.44% of the revenue.

- Class C items make up for 45% – the biggest share of the total stock units but their share in the total revenue generation is a mere 2.26%.

- Thus, this ABC analysis example clearly corroborates the ABC analysis and underlying Pareto Principle that 80% of the value is contributed by 20% of the items.

Advantages of ABC Inventory Analysis

ABC analysis is quite useful for the organization as it leads to:

1. Optimization of ABC Inventory Management function

It optimizes the inventory management process function using ABC analysis. Each class of the inventory gets management attention as per its value and accordingly, manpower is allocated and expenses are incurred to manage it. It ensures that most important items are regularly monitored and closely observed whereas such efforts are expended with for the less important items.

2. Avoiding loss of business opportunities

As the business is able to identify its most popular and high-value stock items under ABC analysis classification, it can always keep a watchful eye on the movement f these stock items. They will be stocked frequently and sufficiently so as to avoid the situation of stock out and the possibility of turning down the customers is minimized.

Similarly, the business will strive hard to predict the market trends in terms of its high-value items and accommodate any changes in its business strategy so as to capture more customers for its high-value items.

3. Less stock handling costs for low-value items

It is not possible and advisable too, for any business to treat each and every item in its inventory, equally. ABC analysis facilitates the management of inventory according to the values derived from it. Thus low-value items – they reorder, insurance, and warehouse space – can be managed on low priority, low expense, and automated basis. Personal attention is reserved for high-value items.

4. Opportunity to convert Class B items into Class A

As Class B items hold potential for growth, the business may tap into this opportunity and convert it to frequent yet low-value customers into regular, high-value customers to Class A.

Cautions to be exercised while adopting and accounting ABC analysis classification

- The business may place undue influence on managing the Class A items, due to which less important yet essential Class C items may be ignored and business operations may be affected due to the non-availability of these items.

- The business may fail to adhere to the requirements of ABC analysis in practicality. Though the classification is set, still it may spend lots more time and energy in maintaining its Class C items because of its sheer magnitude, and Class A and Class B will be sidelined. ABC Analysis becomes ineffectual in this case.

Liked this post? Check out the complete series on Distribution

Good afternoon, I am interested in logistics and supply chain management, procurement / purchasing, inventory management. I would mind if I can be getting lecture notes and materials to enhance my career. I look forward to hearing from you.Thanks. Dan Onyema